1.0 PURPOSE

This Roadmap provides an overview of the Eastern Caribbean Central Bank’s (ECCB/the Central Bank) Basel II/III implementation programme for the Eastern Caribbean Currency Union (ECCU). The document outlines the Central Bank’s approach towards implementation, the implementation options selected and key deliverables/activities. The Roadmap is intended to guide the expectations and actions of all stakeholders associated with the Basel II/III implementation process.

2.0 INTRODUCTION

The ECCB is committed to implementing certain aspects of Basel II/III in the ECCU for computing the capital adequacy of institutions licenced under the Banking Act 2015 (the Act), in accordance with Sections 46 and 47 of the Act1. Towards this end, the ECCB established a dedicated team (Basel Implementation Group) for spearheading the implementation effort and a Basel II/III Working Committee comprising of representatives from the ECCB, ECCU Bankers Association and commercial banks, for collaborating with the banking industry on an ongoing basis. The Central Bank sought comments on some draft standards2 in 2018 and plans to continue to deepen its interaction with licensees via a number of consultations and training sessions.

Basel II/III constitutes a more comprehensive measure of capital adequacy than the existing Basel I. Basel II/III seeks to align regulatory capital requirements more closely with the underlying risks that banks face. The framework requires banks to assess the riskiness of their assets with respect to credit, market and operational risks and seeks to ensure that banks’ minimum capital requirements better reflect inherent risks in their portfolios, risk management practices and accompanying disclosures to the public.

The full implementation process will result in the creation of Basel II/III implementation standards; revision of capital reporting forms and the creation of a system for licensed financial institutions (LFIs/licensees) to assess their capital adequacy based on ongoing risks. Full implementation will also result in licensees’ maintaining systems for monitoring and documenting their operational risk loss events and; ultimately becoming more risk-focussed.

3.0 BACKGROUND

The Basel I capital framework is not sufficiently sensitive to account for the risk confronting LFIs in the ECCU. The Central Bank has therefore been considering the merits of adopting some of the newer options put forward by the Basel Committee on Banking Supervision (BCBS)3. With the publication of Basel III, the ECCB found it prudent to adjust its approach to the implementation of Basel II and develop a Basel II/III hybrid approach instead. While the ECCB’s implementation approach is to adopt the principles of the Basel framework, the Central Bank recognises that many areas of the Basel II/III framework are not appropriate to financial institutions in the ECCU, given the relative simplicity of their operations. Therefore, the ECCB will tailor the Basel requirements to the regulatory needs of the ECCU jurisdiction.

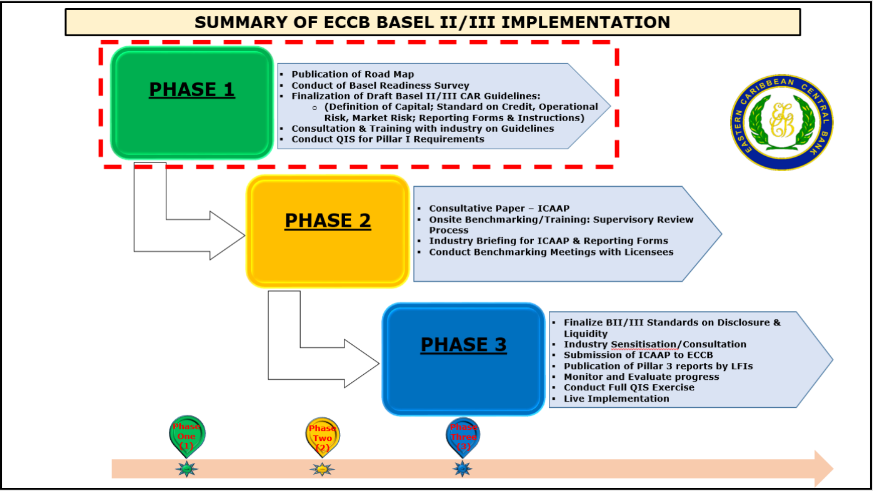

4.0 PHASED APPROACH TO BASEL II/BASEL III IMPLEMENTATION

The ECCB will implement its Basel II/III framework in three (3) phases. The first phase will involve the implementation of the Pillar I framework, the second phase will focus on the implementation of Pillar II and the third will include the implementation of Pillar III. Appendix I outlines the implementation activities envisaged for Phases 1, 2 and 3.

4.1 PHASE 1: IMPLEMENTATION OF BASEL II/III PILLAR I

Pillar I - Calculation of the Minimum Capital Requirements

Pillar I seeks to align the minimum capital requirement more closely with banks’ credit, market and operational risks. The ECCB will allow banks to utilise the following methods for capital computation under the Basel II/III framework: the Basel III Definition of Capital, the Basel II Standardized Approaches for Credit Risk and Market Risk, and the Basic Indicator Approach for Operational Risk.

The three major implementation deliverables under phase 1 will include:

-

Finalisation of the draft Standards.

-

Industry consultations and training.

-

The undertaking of a Quantitative Impact Study (QIS) utilising prudential reporting forms and guidelines:

a) Finalization of the draft Standards

The following Basel II/III standards are being finalised for submission to the industry:

- Standards on the Definition of Capital;

- Standards on Credit Risk;

- Standards on Operational Risk; and

- Standards on Market Risk.

b) Consultations and Training

The implementation of Basel II/III will constitute a major paradigm shift and require significant effort from all stakeholders during every phase of the implementation process. In Phase 1, the ECCB will:

- Hold consultations with licensees to outline our approach to implementation.

- Examine some of the related technical issues4

- Respond to industry inquiries and highlight regulatory expectations.

The ECCB established a Basel Working Group to work on Basel II/III implementation matters on an ongoing basis and continues to pursue avenues for long-term technical assistance (TA).

c) Quantitative Impact Study

As a tool, the Quantitative Impact Study (QIS) will be used to assess the impact of the new Basel II/III requirements on the quality and level of capital assuming full implementation. This will involve application of the new Basel II/III capital structure and Pillar I capital measures for Credit, Operational and Market Risk. The QIS will primarily examine the changes to LFIs’ capital (based on the Basel II/III framework), changes in overall risk-weighted assets and the impact on LFIs’ capital adequacy ratios. It will collect more detailed information than is currently available in prudential reporting or from other sources. The QIS will also enable the ECCB to complete a desktop assessment of the impact of the new Basel II/III requirements to determine levels of proportionality and discretion. The study will be accompanied by the necessary guidance and will be preceded by a qualitative questionnaire. The ECCB will invite LFIs to participate in this exercise.

The sector consultation and QIS will contribute significantly to finalising the policy positions reflected in this document. Licensees are therefore encouraged to submit comments to the ECCB for consideration.

4.2 PHASE 2: PILLAR II

The Supervisory Review Process

During the Supervisory Review Process, the ECCB will verify whether licensees have adequate systems in place to identify, measure and manage the risks relevant to their risk profile and whether they maintain sufficient capital to cover other risks not specifically covered under Pillar I. The additional risks for which the Central Bank may prescribe capital include credit concentration risk, interest rate risk in the banking book, liquidity risk, strategic risk and reputational risks. The ECCB will review and evaluate banks’ Internal Capital Adequacy Assessment Process (ICAAP) and strategies, as well as their ability to monitor and ensure that the capital held, is commensurate with their risk profiles.

Under the Supervisory Review Process, licensees’ directors and senior management are responsible for implementing internal procedures for assessing capital holdings and goals in line with their business risk profile and internal management and control systems. Pillar II is based on four interlocking principles:

- Principle 1: LFIs should have a process for assessing their overall capital adequacy in relation to their risk profile and a strategy for maintaining their capital levels – an ICAAP.

- Principle 2: The ECCB will review and evaluate licensees’ ICAAPs and strategies, as well as their ability to monitor and ensure their compliance with regulatory capital ratios. Appropriate supervisory action will be taken, if the ECCB is not satisfied with the result of this process.

- Principle 3: The ECCB expects licensees to operate above the minimum regulatory capital ratios and will require licensees to hold capital5 in excess of the minimum.

- Principle 4: The ECCB will take action at an early stage to prevent capital from falling below the minimum levels required to support the risk characteristics of a particular licensee and will require rapid remedial action if capital is not maintained or restored.

As part of the capital adequacy process, LFIs will also be required to develop board approved contingency capital restoration plans to address any capital deficiency issues.

4.3 PHASE 3: PILLAR III

Pillar III reinforces Pillars I and II, through the use of increased disclosure requirements. These disclosures will enable the public to assess the capital adequacy of licensees and therefore empower them to exert market discipline on financial institutions. Licensees will be required to make public discloses regarding key information on capital, risk exposures, risk assessment processes and hence the capital adequacy of the institution. The disclosures will enable market participants to better assess the safety and soundness of banks and thus impose stronger market discipline on banks’ behaviour.

Licensees will be required to publish information on their approach to risk management, thus raising the standards of transparency in the Eastern Caribbean Currency Union (ECCU) financial environment.

5.0 CONCLUSION

The ECCB is proceeding with its Basel II/III implementation programme, given the shortcomings of the current Basel I capital framework. The implementation of Basel II/III will significantly enhance risk capture by licensees, improve the robustness of capital and enhance the ECCU financial system. The implementation of Basel II/III constitutes a major undertaking and will therefore be carried out via a phased approach. In moving forward, the ECCB will: engage licensees; seek their comments; and provide training and guidance, where and when possible. Licensees should commit appropriate personnel and resources to this Basel II/III project and pledge their commitment to work with their regulator in order to see the project to fruition.

APPENDIX I

BASEL II/III IMPLEMENTATION ROADMAP: PHASE 1